Don't Throw Away Your Money

No intro necessary for this one... we're just going to jump right in to the facts.

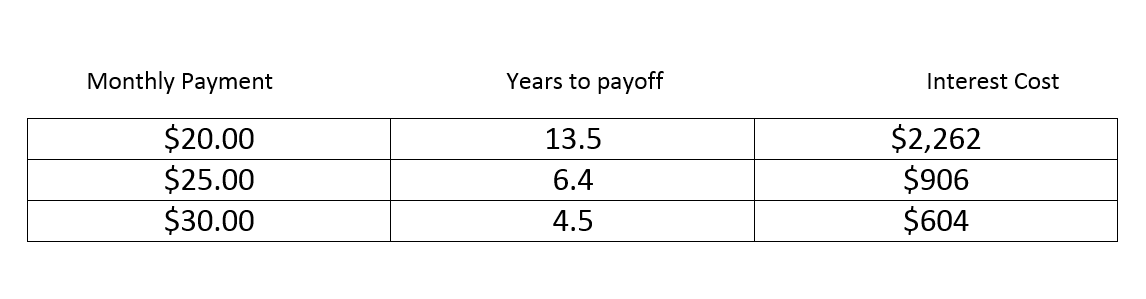

If you owed $1,000 at 22.90% APR, here is the breakdown:

That "innocent" little credit card you took out to cover Christmas gifts might not have been the best deal after all.

You think "Twenty dollars a month is nothing - that will be easy to pay off." Then you realize it's not so easy or cheap; making the minimum $20 payment will take you 13 years to pay off. And it will end up costing you twice as much!

The good news is knowing is half the battle. If you pay more than the minimum payment, you'll pay down your debt faster and pay a lot less in interest charges.

What changes can you make to your spending so you can send an extra $5, $10, or even $15 a month on this bill? Can you skip your coffee run once a week? Pack your lunch instead of dining out?

In the example above, it goes to show you that even paying a little bit more will save you hundreds of dollars in the long run! Also, if you will be getting a tax refund, consider using part of it to pay a chunk or completely pay off that credit card.

But make sure you first prioritize where that money should be used. If you are struggling to find money to make higher than minimum payments, then a Debt Management Plan may be a better option.

If you sign up for a DMP, the debt included will be paid off in five years or less and will have a fixed and likely lower interest rate.

To find out if a DMP is right for you, call LSS at 888.577.2227 for your financial counseling session. Or you can begin your online session now by clicking below. Either way, your session will be free and confidential. Don't debt let take over your life; take action today to eliminate it for good.

Author Katie Eastman is a Certified Financial Counselor with LSS Financial Counseling and she specializes in budget, credit, and debt counseling.