529 College Savings Plans: Part II

In the first installment about 529 College Saving Plans, I discussed the basics about those plans to give you an idea what they’re all about. This post focuses on the best features such plans have to offer.

In the first installment about 529 College Saving Plans, I discussed the basics about those plans to give you an idea what they’re all about. This post focuses on the best features such plans have to offer.

Benefits of 529 Saving Plans:

529 plans are designed to encourage early and consistent savings by offering an affordable and convenient way for families to save for college. While the tax advantages are one of the primary benefits, states also offer a variety of additional benefits to help families reach their college savings goals. These benefits include:

- All money grows federal and state income-tax free

- All withdrawals used for “qualified higher education” expenses are exempt from federal income tax

- Many states also exempt withdrawals from state income-tax for “qualified higher education” expenses (so check your state’s specific plans)

- The account holder retains control of the assets

- Many plans have low minimum monthly contribution limits so there are options for families regardless of income level

- Money can be used at most accredited colleges across the country

- Money can be used for tuition, fees, room, board, books, supplies and required equipment (depending on the type of plan – see chart below)

- Contributions can be made conveniently through payroll deduction or automatic transfers from a bank account

- Many states offer maximum contribution limits of $300,000 or more

- Assets within 529 plans are protected from bankruptcy

- Most states offer a low cost option that can be opened by contacting the plan directly

- 529 plans are also offered through professional financial advisors who can help you choose a 529 plan and an investment strategy to meet all your needs (see more at www.finra.org)

To give credit where it is due, you should know that the summary above and the chart below were found at www.sec.gov.

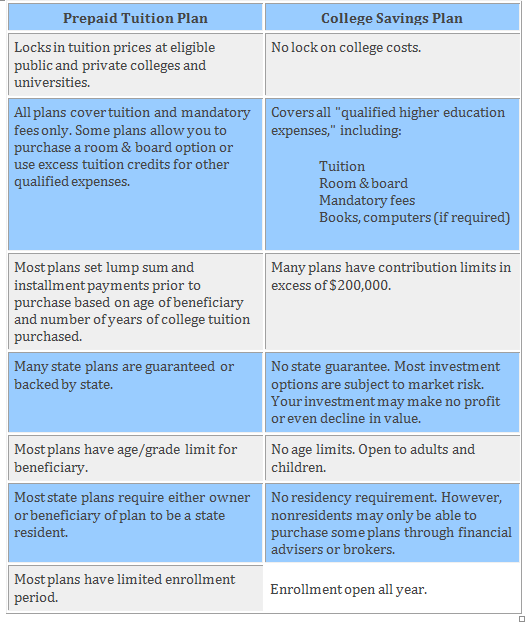

This SEC chart outlines some of the differences between the Prepaid Tuition Plan and the College Savings Plan for easy comparison:

Remember, all funds must be used for qualified education expenses to be eligible for the tax benefits associated with 529 plan. If you withdraw funds for any other reason, you will be subject to tax consequences that may be significant. Best to plan on using the funds for college costs only. If you have other financial goals or priorities, this may not be the time to invest in a 529 college savings plan.

In a future post, I will discuss this as well as other considerations to think about before investing in a 529 plan.

Give us a call at 888.577.2227 and ask to schedule a student loan appointment. The counseling is a free and confidential. A student loan expert can take a look at what’s really going on with your loans and get you on your way to successful repayment.

Author Barbara Miller is a Bankruptcy Specialist and Financial Counselor at LSS Financial Counseling. Have a question for Barb? Email us as financialcounseling@lssmn.org